Options Pricing

Introduction

In this section we will introduce options, a widely used financial instrument used for a range of purposes, such as protecting traders from risk and speculating on the price movements of assets. We will introduce options, outlining their properties and describing a procedure for calculating their price. In later sections, we will apply this procedure multiple times, culminating in the famous Black-Scholes equation, and discuss the practical implications of trading options.

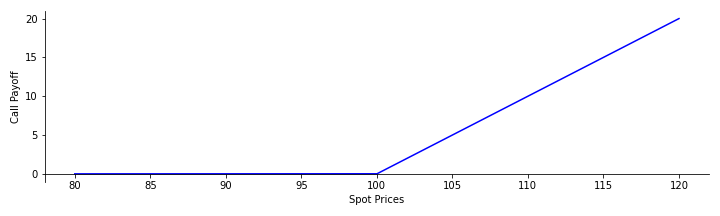

An option is a contract which gives its owner the right, but not the obligation, to buy or sell a specific quantity of an underlying asset or instrument at a specified strike price on or before a specified date. There are many types of option; we will consider only the basic options in this course: calls and puts. There are also two types of expiry: European options can only be exercised at expiry, whereas American options can be exercised any time up to expiry. A call option gives its owner the right, but not the obligation, to buy a specific quantity of an asset at the strike price on or before the contract expiry. Let's break down what this means; Suppose we have a stock, $S$. Let the price of the stock at a time $t$ be $S_t$. Suppose we hold a call option with strike price, $K$, and expiry $T$. If the stock price at the contract expiry, $S_T$, is greater than the strike price, $K$, then we get to purchase the stock at price $K$ and sell it again at $S_T$, gaining the difference. If however the stock price at contract expiry is less than the strike price, we get nothing. Since we have the right but not the obligation to exercise the option, and exercising the option when $S_T < K$ will lose us money, we choose not to exercise it. So, the payoff is $$ \text{Payoff}_{\text{call}}(S_T) = (S_T - K)_+. $$ The '+' subscript indicates that we only consider the positive values of the function, with negative values being equal to zero (that is, we do not exercise the option). A plot illustrating the payoff of a call option with strike $K=100$ is shown below.

The payoff of a call option at option expiry

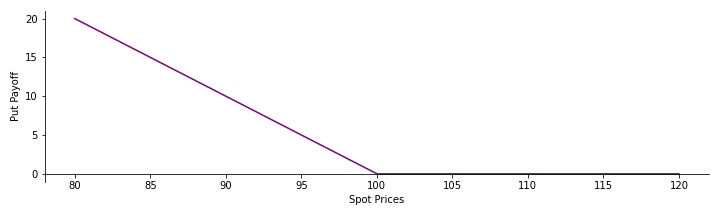

Similarly, a put option gives its owner the right, but not the obligation, to sell a specific quantity of an asset at the strike price on or before the contract expiry. Let's break this down in a similar fashion as before; Suppose we have a stock, $S$. Let the price of the stock at a time $t$ be $S_t$. Suppose we hold a put option with strike price, $K$, and expiry, $T$. If the stock price at the contract expiry, $S_T$, is less than the strike price, $K$, then we get to sell the stock at a price $K$ and purchase it again at $S_T$, gaining the difference. If however the stock price at contract expiry is greater than the strike price, we get nothing. Since we have the right but not the obligation to exercise the option, and exercising the option when $S_T > K$ will lose us money, we choose not to exercise it. So, the payoff is $$ \text{Payoff}_{\text{put}}(S_T) = (K - S_T)_+. $$ A plot illustrating the payoff of a put option with strike $K=100$ is shown below.

The payoff of a put option at option expiry

Pricing Options

In the previous section we knew the option payoff because we already knew the asset price at expiry, $S_T$. If however we attempt to value a call option before expiry, then what information can we use? By pricing an option before expiry, we must find some way of calculating an expected payoff of an option. The price of an option should be equal to its expected payoff. If it isn't we can create an arbitrage portfolio and get a risk-free profit. We must consider a range of potential terminal asset values, $S_T$ and assign a probability to them. Then, we can calculate the value of an option $$ E[\text{Payoff}] = \sum_{S_i} \text{Payoff}(S_i) P(S_T = S_i) $$ where $P(S_T = S_i)$ is the probability that the asset value is equal to $S_i$ when the option expires. How can we determine appropriate values of $P(S_T = S_i)$? We can do so by using an appropriate mathematical model for the underlying asset. In the next sections we outline the common models for pricing options, culminating in the famous Black-Scholes equation.