Trading

Market Making

Market makers have come to dominate a region of finance, and generate huge profits and compensation for their employees. In this section, we outline the concept of market making and how market making firms generate profit.

Another common type of trading strategy is market making. This strategy was originally carried out in the 'open outcry' style, in trading pits, and the automation of this strategy directly led to the birth of many modern, successful high-frequency trading firms, such as Optiver and Susquehanna. Proponents of this strategy place limit orders passively — bids below the current best offer, and offers above the current best bid — in an effort to trade against price-insensitive market participants who cross the bid-offer spread. Since this strategy relies on waiting for others to trade, it is qualitatively different from an arbitrage strategy.

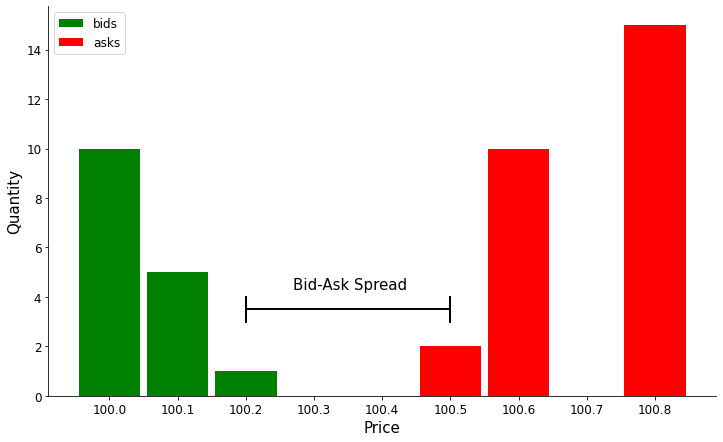

A graph illustrating the limit-order book.

For example, here we could place a bid at the best bid and an offer at the best offer. If things go well, a seller will arrive in the market, and a buyer at around the same time, and we will buy at the best bid and sell at the best offer, making a small profit equal to the bid-offer spread.

It is irrational to place an order at a price worse than you think is fair for that product; in other words, all of our orders need positive edge, which is the expected profit of the order, measured against its fair price:

$$\text{edge} = \begin{cases} \text{fair price} - \text{order price}, & \text{for bids} \\ \text{order price} - \text{fair price}, & \text{for offers} \end{cases}$$

In particular, say we think the fair price of the above product is the mid-price. We could then also place a bid one tick above the best bid and an offer one tick below the best offer, and our orders would still have edge. These orders would have less edge than the first set, but better price priority, making them more likely to trade quickly and generate a profit.

Let's take a step back to see what has happened here. By providing orders for others to trade against around our fair price:

- We have contributed to the consensus mechanism that establishes this product's fair price.

- With the second set of orders, we have actively improved the best price at which transactors can trade.

- Even with just the first set, we have added book depth: if somebody wishes to transact a large size, they will match against more quantity at a better price, improving the average price of their transaction.

Through all of these methods, market makers contribute to the efficient functioning of the markets.

A market maker estimates that a product has a fair price of 100. The tick size is 0.1. At what price should she place her bid in each of the following two markets?