Trading

Arbitrage

Here we introduce the concept of arbitrage - a simply yet widely used trading strategy that exploits price mismatches between trading venues.

Arbitrage is a common trading strategy exploited by a wide range of trading firms, and involves exploiting price discrepancies between different venues. Arbitrage traders monitor the same asset on multiple venues. Assets are traded on various venues, and the prices for the same asset can vary due to factors such as market demand and the liquidity of an asset on a particular venue. Suppose there are two exchanges, $A$ and $B$, both trading a particular asset. The asset on exchange $A$ is very liquid and the one on exchange $B$ is much less liquid. If the price on exchange $B$ disagrees with the price on exchange $A$, it is most likely because the asset is not priced correctly on exchange $B$. If the asset is being sold cheaper than it is being bought elsewhere or vice versa, trading firms can exploit the disagreement to gain a profit. This profit does not come with zero risk however, as market prices can rapidly change. Trading firms therefore have to act as quickly as possible to capitalise on the opportunity before price equilibrium is restored and before competitors seize the same opportunity. Since these opportunities are easy to spot and short-lived, it is typical for trading algorithms to be constantly monitoring exchanges to detect and execute exchange arbitrage without human intervention.

Notice the effect of arbitrage trading on the market — in both cases, the prices of the related markets have returned to being in line, and the arbitrageur has provided price efficiency to the market.

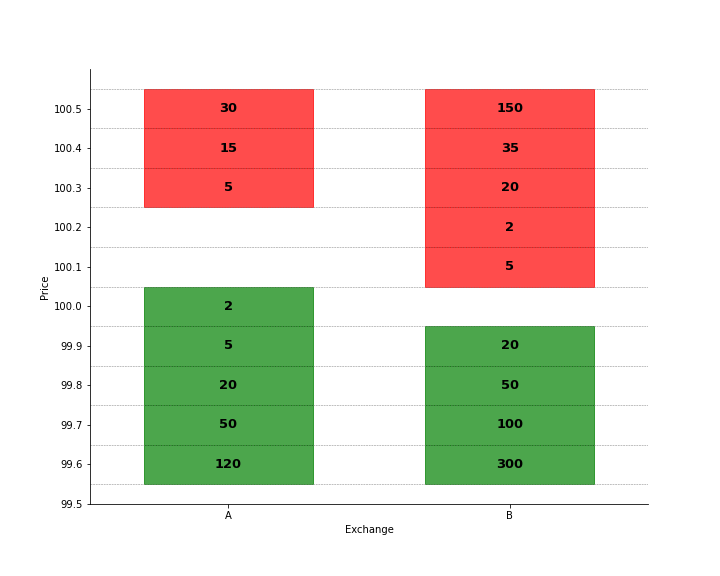

Consider the limit-order books for exchanges $A$ and $B$ below.

1. Limit-order books of exchanges $A$ and $B$.

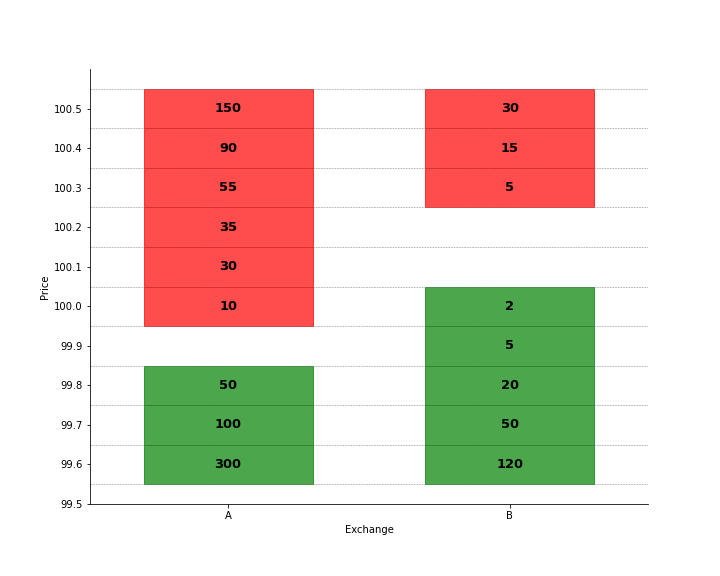

Let's consider another example.

2. Limit-order books of exchanges $A$ and $B$.

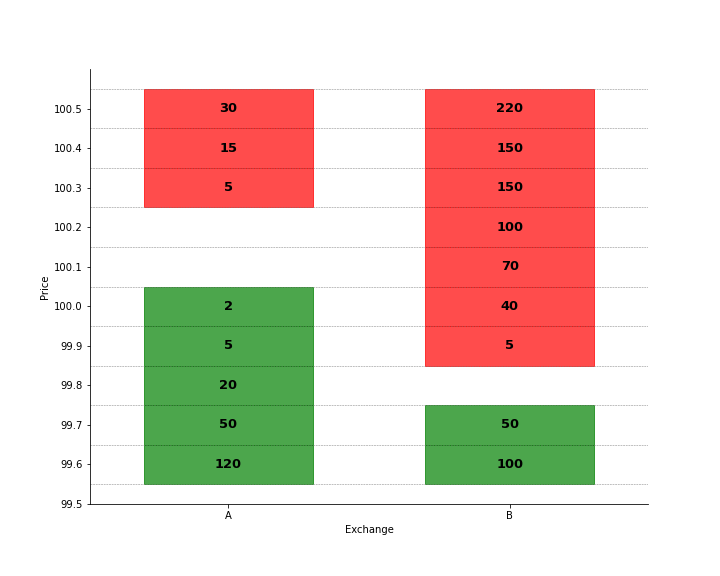

Let's see a final example.

3. Limit-order books of exchanges $A$ and $B$.